King of the Business Case

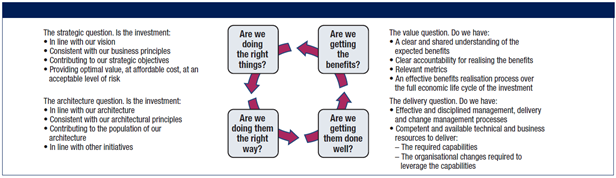

16th of October 2015At some point in any IT architect’s career, he will be asked to write up a business case, proving the worth of an initiative before proceeding to invest in it. There are several frameworks to do this, like for example the Val IT Framework of COBIT. This framework elaborates on business cases using four simple questions (with no so simple answers), as shown in the illustration below. As a comprehensive framework for the design and delivery of high-quality IT-based services, COBIT sets good practices for the IT function's means of contributing to the process of value creation. Val IT sets good practices for the ends (the outcomes) thereby enabling enterprises to measure, monitor and optimise value, both financial and non-financial, from IT-enabled investments.

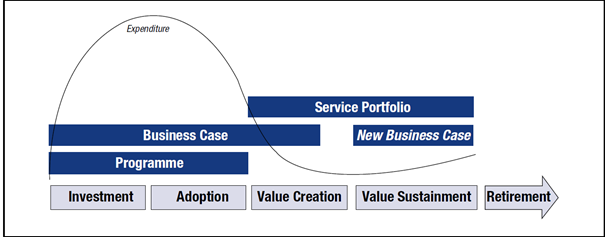

All initiatives have an intended lifespan, which is frequently set to a 3- or a 5-year time period, divided as indicated by the graph, partitioning the period in 5 segments. These segments have linked to them, a level of expenditure before the value of the initiative can be realized and sustained for profitability.

The question “Are we getting the benefits?” is where we attempt to calculate the value created, in order to weigh it against the cost of implementing the initiative. These benefits come in different forms:

1. Hard Benefits: The hard numbers. How much money is generated or saved by the initiative?

2. Soft Benefits: Bottom line improvement where we cannot easily quantify

3. Strategic Benefits: Capability development in order to further strategic initiatives or to meet a business objective

4. Operational Benefits: Capability development in order to support the operational side of the enterprise or to meet an operational objective

Many pages can and already are written on this, but in this article, I want to focus on the hard or quantifiable benefits. For this, I can’t help but notice we always seem to fall back on the Return On Investment, or ROI (which happens to be the French word for king, hence the title of the article). In very basic terms, this boils down to the profit divided by the investment. However, in business cases, this becomes the net return, or the profit minus the investment. However, there are some drawbacks to this rather simple approach, prompting the evaluation of other forms of benefit calculation.

One of those drawbacks is the fact it is an absolute value, while most initiatives, as stated earlier, have a lifespan of several years. In order to take this into account, the concept of a Net Present Value (or discounted cash flow stream) rears its head. Here we take into account not only the cost of the investment, but also the cost of procuring the funds as well as the simple fact that money now (the present value of this investment) is much more precious that the equal amount when it is earned back through the initiative in later years.

To illustrate this, we assume that the present value of funds will take a 10% dip each year. This gives the following calculation that for a 100K € return after three years, to have equivalent value now, the investment can only be 100K € divided three times (for each year) by 1,10, we arrive at an initial investment value of 75131 €. This represents the Present Value. However, to calculate the Net Present Value you need to subtract the investments, and add the returns.

Let’s start with an investment of 200K €, with no additional investments and a return of 10K € every year, and a payout of 250K at the end of the third year. Suppose there is a 10% interest rate at banks. This gives us the following progression, indicating it is a profitable initiative:

Year 1: PV = € 10K / 1,10 = € 9.091

Year 2: PV = € 10K / 1,10² = € 8.264

Year 3: PV = € 10K / 1,10³ = € 7.513

Year 3 (final payment): PV = € 2.500 / 1,10³ = € 187.829

NPV = € -200K + 9.091 + 8.264 + 7.513 + 187.829 = € 12.697

Another drawback of ROI is the fact it does not take into account the risk factor of the investment. Where we use a static 10% in the NPV calculation, a more appropriate value could be used. For this reason, we could employ a Weighted Average Cost of Capital, or WACC. If not available in an organization, this can be calculated with the following formula:

The parameters used in the formula are as follows:

Re = cost of equity

Rd = cost of debt

E = market value of the firm's equity

D = market value of the firm's debt

V = E + D = total market value of the firm’s financing (equity and debt)

E/V = percentage of financing that is equity

D/V = percentage of financing that is debt

Tc = corporate tax rate

If not known for your enterprise, and not easily calculated, it is also possible to simulate this in your calculations but using a conservative estimate of ROI and aggressive estimate of ROI. The difference between these two, as they use the same cost basis, will signify your spread of reasonable expectations to use in the calculation of your NPV.

I hope to have illustrated to you that there are many other calculation models out there for your business case beyond the simple ROI calculation and that we shouldn’t shy away from these, even though they are more elaborate. They also paint a better picture of the returns and how to assess the value of these returns. For more information about such methods, this website by Aswath Damodaran is a very good resource.

Finally, I leave you with a link to an Excel with these two models and their calculations ready to use in the documents section of the website.

| Thought | Business Case |